Many of my friends & relatives hold an SBI credit card and its usually the SBI IRCTC Platinum Credit Card because most of them travel at least once a month via train between their native and work location. As it helps to save upto 10% on IRCTC spends, its definitely a worthy card to hold. Let’s see in detail below:

Joining Fees

Joining/Renewal Fee: Rs.500+GST

Welcome Benefit: 350 points

The welcome benefit kind of sets off the fee partially, which makes Sense for a low fee card with a very good return on spend on IRCTC train bookings.

Rewards

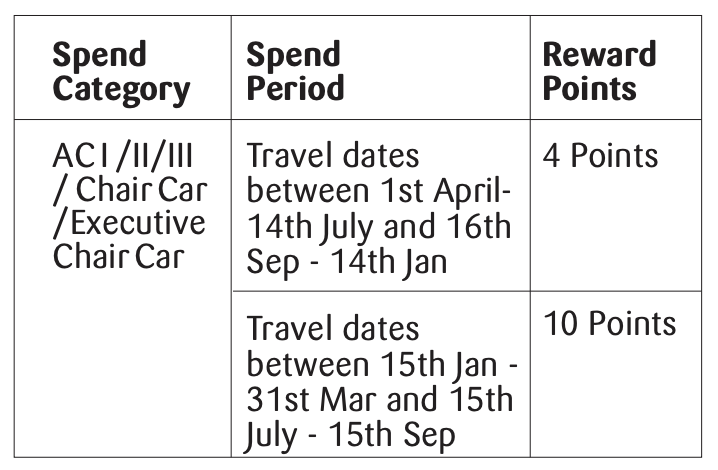

IRCTC Train Bookings – Peak Season: 10% as points (AC1, AC2. AC3 and AC CC)

IRCTC Train Bookings – OFF Season: 4% as points (AC1, AC2. AC3 and AC CC)

All other spends: 0.8% as points (1 Reward point for every Rs. 125)

1 Reward point = Rs.1

Note: To be eligible for the rewards, booked ticket must have one Traveller same as the name on the card

Save 1.8% transaction charges on railway ticket bookings

1% fuel surcharge waiver, on txns of Rs. 500 – Rs. 3,000, exclusive of GST and other charges (maximum surcharge waiver of Rs. 100 per statement cycle)

Bottomline

Rating: 3.8/5 [yasr_overall_rating]

Its a very basic one and was indeed an amazing card until the launch of the new, improved & premium version of this card which is SBI IRCTC Premier Credit Card. So it now makes no sense to hold on to the platinum card unless your spends are low (or) your train travel is seasonal and falls under the period where this card gives you 10% returns.

Remember, if you spend less than 20K on train tickets a year, I wouldn’t even suggest you to go for either of the IRCTC cards, you may rather go for the newly launched entry-level cards like SBI Ola card or Axis Flipkart Card or ICICI Amazon Card which could get you rewards on all type of spends.

Do you have IRCTC Platinum credit card? Feel free to share your experiences in the comments below

SBI offers very few premium credit cards and SBI Elite Credit Card is one of them. It stands between Sbi Prime (semi-premium card) and SBI Card Aurum (super premium card).

It was previously issued as SBI “Signature” Credit Card long time ago, which I was holding for sometime before they devalued it and made it as SBI Credit Elite. Here’s everything you need to know about the SBI Elite Credit Card in it’s current form.

Overview

Type

Premium Credit Card

Reward Rate

0.5% – 2%

Best for

Milestone benefits

USP

Movie benefit

SBI Elite Credit Card is a decent premium credit card, which is good for those who prefer milestone benefits along with the lucrative monthly movie benefit.

However, SBI Elite Card shouldn’t be a choice for most, which you’ll know why shortly.

Joining Fees

Joining Fee

4,999 INR + GST

Welcome Benefit

Rs. 5,000 e-gift Voucher

Renewal Fee / Annual Fee

4,999 INR + GST

Renewal Benefit

Nil

Renewal Fee waiver

On spending >10 lakhs

Welcome Gift Voucher Options: Yatra, Hush Puppies/Bata, Pantaloons, Aditya Birla Fashion and Shoppers Stop.

When it comes to renewal, if the renewal spend criteria is met, they usually charge the fee & then refund it back after a week. I wish they rather not charge at all, just to avoid confusion.

To apply, You’ll need to open the link on desktop (not mobile), click on “start apply journey” and click on “change card” and choose your preference.

Design

I’ve had a look at the SBI Elite Credit Card in person multiple times in the last few years and it looks beautiful for sure.

Rewards

SPEND TYPE

REWARD POINTS

REWARD RATE

Regular Spends

2 RP / 100 INR

0.50%

Dining, Departmental stores & Grocery Spends

10 RP / 100 INR

2.5%

1 Reward Point Value: Rs.0.25 (can be adjusted as statement credit)

Category exclusions apply, just like most other SBI Cards

Milestone Rewards

Annual SPEND

MILESTONE Benefit

SAVINGS (Cumulative)

Reward Rate

3 Lakhs

10,000 Points (2,500 INR)

10,000 Points (2,500 INR)

0.8%

4 Lakhs

10,000 Points (2,500 INR)

20,000 Points (5,000 INR)

1.2%

5 Lakhs

15,000 Points (3,750 INR)

35,000 Points (8,750 INR)

1.7%

8 Lakhs

15,000 Points (3,750 INR)

50,000 Points (12,500 INR)

1.5%

The spend-linked milestone benefit is the key feature of the SBI Elite Credit Card, as this alone can offer a return of 1.5% on 8L annual spends.

And if you add the regular rewards, assuming 0.5% on regular retail spends, that’s a decent 2% reward rate.

Not to forget that SBI Signature credit card (no more available) used to offer a 3% reward rate with which I earned Rs.18,000 Cashback in the past.

Max Tickets: 2 per month, 250 INR/ticket = 500 INR savings a month

Complimentary movie tickets worth Rs.500 per month is an excellent benefit on this card and is undoubtedly the favourite benefit for most Sbi Elite Cardholders.

Airport Lounge Access

ACCESS TYPE

ACCESS VIA

LIMIT

Domestic (Primary)

Visa / Mastercard

2/Qtr

International (Primary)

Priority Pass

6 (Max: 2/Qtr)

Remember, both lounge benefits applies only for Primary SBI Prime Credit Card holder and not to forget that the Priority Pass expires in 2 Years.

Other Benefits

Fuel Surcharge Waiver: Enjoy 0% surcharge (Minimum transaction of INR 500. Maximum waiver of INR 250 per statement cycle)

Foreign Exchange Markup fee: 3.5% + Service Tax

Club Vistara Silver & Trident Red Tier membership

Golf sessions via Mastercard World benefit.

Personal Concierge Service: Global Concierge Assistance for all your travel & other needs. Its kind of virtual assistant service over phone.

The concierge service available with this card is the same as that provided on SBI Aurum Credit Card. Though I’m unsure if they’re still providing it on Elite cards.

Should you get it?

Quick answer: No

Long answer: If you’re a movie buff who can take advantage of the benefit every month, I think it’s a decent card. Let’s see how the reward rate changes with the Movie benefit:

You get 2% return on 8L regular spends

You get 1.35% return on 10L regular spends (with annual fee waiver)

You get 2% return on 10L spend + if you avail movie benefit every month

So the maximum return that you could get from the card is only 2%, which is too low in 2024 for 10L annual spends.

In most cases that I’ve personally seen, if one has higher spends of about 10-12L a year and looking for a best SBI Card, then SBI Aurum Credit Card is a much better choice over SBI Elite Credit Card any day.

But of-course if you’re not eligible for Aurum Card and still need movie benefit, then SBI Elite Credit Card might just serve the purpose.

To apply, You’ll need to open the link on desktop (not mobile), click on “start apply journey” and click on “change card” and choose your preference.

Bottomline

Rating: 3/5

While the SBI Elite Credit Card was a decent option in the past especially due to it’s movie benefits, I don’t think it’s a preferred choice in 2024.

The Cashback SBI Credit Card now offers a straightforward 5% cashback on online spends, and even the SimplyClick SBI Credit Card that comes at a very low fee provides a sweet 5% return on 2L annual spends.

These 2 cards are a gem not only within SBICards but also across the banks in India. If your spends are on the higher side, you should explore Aurum SBI Credit Card which comes at a pretty good reward rate on 1L monthly spend.

Do you think SBI Elite card is for you? Do share your views in comments below.

HSBC Visa Platinum Credit Card: I’ve been asked to review the HSBC Credit cards for couple of years now but i had always postponed it as i thought HSBC would go out of business. Well, I read somewhere few years back that HSBC isn’t interested in getting aggressive on Indian Credit card business so i thought they’ll exit soon.

Fortunately they didn’t. But they’re choosy in issuing credit cards, like, they don’t encourage self-employed individuals. Anyway, i’m happy to finally share the review of their Platinum Credit card with some good insights.

While there are multiple credit cards in HSBC portfolio, i believe HSBC Visa Platinum Card is the only one they’re actively promoting. So this is the review of the same.

Joining Fee/Annual Fee: Nil

The surprising part of HSBC credit cards is that they don’t have any joining/annual fee on any of their cards.

Welcome Offers

Get ₹2000 Cleartrip voucher on first transaction (Limited period offer)

Get 10% cashback (up to ₹2500) for making a minimum of 9 transactions totaling to ₹10,000 or more in the first 90 days.

3X Rewards on Dining, Hotels and Telecom for first 12 months from the date of issuance of your credit card

BookMyShow voucher worth ₹500(2 * 250 voucher) on spending over ₹50,000 in a calendar month. Maximum of ₹3000 per cardholder in a year.

Buy 1 Get 1 Tickets has to be only for Saturday shows but you can book on any day the week. Once in a month. Add on card treated as separate card.

On Fridays you can get Rs.1200 discount for roundtrip and 1200 off on hotel bookings also using CTHSBCFRIDAY. Add on card treated as separate card.

On Sundays you can get maximum of Rs.10000 cashback (10%) for making international flight tickers in MakeMyTrip. Add on card treated as separate.

Swiggy Offers: 50% discount up to ₹125 valid on your first order on Swiggy | 25% discount up to ₹150 valid on your order on Swiggy

30% discount on treebo hotels

Balance Transfer and Loan Facility

They seem to have impressive rates and this is what Mouli has to say: “Though I am preferred customer in HDFC and have priority relationship with other banks but still HSBC is my goto card for all BT and loan as they offer the lowest percentage and processing fee.

Last month for BT it was 10.9% interest and 1% processing fee and they will give you Rs.300 Uber voucher for taking BT and loan from them.”

Reward Points

2 reward points for every 150 except fuel transactions

5 Times (5X) Rewards on subsequent purchases made after crossing spend amount of ₹400,000 in a year up to a maximum of ₹1,000,000 in a year

Ideally, you can get ~45k Points on spending 10L a year.

Redemption Options

This is where you need to put your mind to some use. I wish HSBC made this part easier for everyone.

Catalogue Redemptions

Popular shopping Gift Vouchers available

Expected Reward Rate: 0.25% (normal) to 1% (on 10L spend)

Airline Transfers

Singapore Airlines (1 Reward Point = 1 Kris Flyer Mile)

British Airways Executive Club (1 Reward Point = 1 Avios Mile)

Jet Airways (2 Reward Points = 1 JPMile)

Hotel Transfers

Taj InnerCircle (5 Reward Points = 1 TIC Point)

1 TIC point = ~Rs.5

Reward rate: ~4.5% (only on 10L Spend)

Here are the numbers on Taj Points transfer,

For 45000 HSBC reward points in a year you will get 9000 TIC points. With this, you can get 7 nights stay in Taj Surya Coimbatore or 3 nights in Taj Fisherman’s Cove Chennai

Just like any other Hotel Loyalty program, based on the property, you can maximize the value even more.

Bottomline

So I have mixed views on this card as extracting value from it isn’t easy unless you’re into the points game. Airline transfers & Hotel transfers are the only ways to get handsome returns and suits only for those who could put 10L spend a year on it, nothing less, nothing more!

Rating: 3.5/5 [yasr_overall_rating]

Furthermore, if you club it with HSBC Offers you may get even more value, but it is overall far away to be called as “rewarding” for the regular cardholders.

Do you hold HSBC Credit Card? Feel free to share your experiences in the comments below.

While American Express is known for their premium cards with amazing customer support they also issue one of the highly rewarding entry-level credit card in the country in the name of Membership Rewards Credit Card (MRCC).

Even though its an entry-level credit card, you can get return on spend as good as any other super premium credit card and even more. Let’s see how.

Overview

Type

Entry-level Card

Reward Rate

1% – 10%

Best for

Gold Collection redemptions

USP

Monthly Reward Milestones

American Express Membership Rewards Credit Card is a pretty decent rewards card that gives lucrative reward rate if used right.

If you’re new to credit cards (holding at-least one non-Amex card) and looking for a higher reward rate to begin your journey, you may start with Amex MRCC.

*** Most loved Amex Card for beginners ***

Apply through the link on the page & you’ll get additional 2,000 Referral Bonus Membership Rewards® points (spend INR 5,000 within 90 days)

Fees

Joining Fee

1,000 INR+GST

Welcome Benefit

4,000 MR Points + 2,000 MR Points (Limited Period Offer)

Renewal Fee / Annual Fee

4,500 INR+GST

Renewal Benefit

Nil

Renewal Fee waiver

Nil

Note that 4,000 MR points are easily valued at 2,000 INR and on top of that, with the limited period offer you get an additional 2,000 MR points (valued at 1,000 INR) when applied through the referral link. So that’s like getting 3X the value overnight.

Further, the renewal fee can as well be waived off by calling Amex support. Expect 100% waiver on renewal with annual spends >1.5 Lakhs. Else, you can get 50% waiver on spends >90K INR.

Design

While I’m not a fan of this yellow credit card, it does look decent after you look at it so many times and get used to it.

Anyway, it’s not about the design that matters for an entry-level card. It’s all about rewards and it does offer quite a lot of that.

Rewards

SPEND TYPE

REWARDS

REWARD RATE (CASH CREDIT)

REWARD RATE (MARRIOTT/TAJ VOUCHER)

Regular Spends

1 MR on every 50 INR spend

0.50%

~1%

Excluded spends: Utilities, Fuel spends

Rewards don’t expire.

If you plan to use the card primarily for fuel and utilities, you may instead have a look at the Amex Gold Charge Card.

The reward points earned on MRCC are ideally meant for Marriott transfers (or) Taj voucher redemptions via Amex Gold Collection (24K), as other options are not attractive enough, unless you know what you’re doing.

Also note that the MR points earned on MRCC can be pooled with other Amex cards (except Plat travel which happens rarely), so you can get closer to 24K or 18K Gold collection redemptions faster.

1 MR Point = ~0.50 INR (average taken for calculation above)

MR Point value can vary from 0.38 INR to 0.58 INR depending on the redemption.

Monthly rewards is the USP of Gold cards (Gold Charge Card & MRCC) wherein customers are given bonus MR points on completing certain spend criteria in a calendar month.

Unlike Gold Charge Card that can get you only 1000 MR points monthly, here with MRCC you can get 2000 MR points every month on completing two spend targets, as mentioned above.

Note that the bonus MR points on 20K spend is an “enrolment based benefit”. So donot forget to enroll.

The Value of 2000 MR points is only 500 INR if you redeem for cash credit but if you aim for the gold collection (or) redeem points at Marriott properties that’s easily 1000 INR value which means you’re getting ~5% return on spend (20K spend).

You may as well accumulate points and hope to redeem for Taj vouchers under 24K Gold Karat Collection which will further enhance the point value from to 0.58 INR.

You may as well get the Gold Charge Card, link both cards and get closer to your redemptions faster, as mentioned earlier.

Amex Offers

One of the major advantage of holding an American Express credit card is that you get access to most of the Amex network offers that shows up from time to time.

This could be merchant offers, spend based offers or even points transfer offers. Check out all previous noticeable Amex Offers here.

While Amex merchant offers used to be AMAZING in the past (2018 & before), we didn’t see much in 2023/2024, but they did multiple decent spend linked offers worth considering.

Amex offers is just one reason for holding an American Express Credit card. Here are 5 Reasons Why You Should Have an American Express Credit Card otherwise.

Reward Multiplier

While Amex Reward Multiplier is something I’m not happy with since it’s inception, it does offer a great value if you’re not into other bank’s Super Premium Credit Cards.

You can get 2X rewards on the Reward Multiplier with Gold Charge Card.

What this means is, you get 1% more reward rate on the spend. While this is not so lucrative as the 5X rewards on Gold Charge Card, it’s still decent enough to get little beyond the regular rewards.

Other Benefits

Foreign Exchange Markup fee: 3.5% + Service Tax

Amex health insurance benefits (with ICICI Lombard)

Supplementary Card Offers

Amex Festive Offers

24/7 premium support

The downside however is that being an entry level card, chances of it being used by non-premium cardholders is high as so are the merchants, due to which one might get into card acceptance issues.

Maximizing MRCC

Monthly Bonus rewards of 2000 MR points (1000+1000) is all you need to consider to earn points faster and redeem for Gold collection.

You may as well explore Points transfer partners if you can flex your mind into the ocean of points & miles game. That said, Marriott points transfer is the easiest one among.

On spending 20K every month you end up getting 24K MR points on 2.4L spend which is a sweet ~6% reward rate.

And if you’ve a flexible travel schedule and can find sweet spots with Marriott (not tough), you may even get value as good as 1 INR per MR point and that my friend means this card can get you a return of 10% annually (on 2.4L annual spend)

Check-out my Marriott Hotel reviews to get some ideas.

Not only it looks lucrative, but also you may enjoy a renewal fee waiver as well with above spends.

If you’re not into travel redemptions, you may as well redeem for other options under Gold Collection like Tanishq or Shopperstop which is quite good as well.

Note: If spending 1.5K*4 is tough for you, you may also load your wallets (if free) or simply split your >3K spends into multiples of 1.5K to get there faster.

How to apply?

You may apply online/offline or at airport outlets (no special airport offers at the moment), whichever is convenient for you.

Currently, one of the best offer you could get is an additional 2K points as Limited period offer when you apply using a referral link.

If you’re already holding an Amex card, do note that American Express allows you to hold 1 Charge Card + 2 Credit cards at any point in time.

*** Limited Period Offer: 2,000 Bonus MR Points ***

Note: It’s better to apply using your Aadhaar address, otherwise the application might get delayed (or) even rejected, as reported by some of those who experienced it.

Bottomline

Rating: 4.8/5

If you’re new to the world of American Express, MRCC is the best card to begin your journey with Amex.

While MRCC is ideally suitable for ~2L or so spends, If your spends are in the range of 4 Lakhs or above, you must check out the Amex Platinum Travel Credit Card which is one of the best travel credit card in the country.

Overall, except for the not so great design, everything else is great with the Amex Membership Rewards Credit Card.

Do you hold American Express Membership Rewards Credit Card? Feel free to share your experiences in the comments below.

If you’re looking for a best travel credit card in India, the American Express Platinum Travel Credit Card is a must have in your wallet. The attractive reward rate on the card is too good to believe and it holds intact even after so many years of it’s existence.

It has been holding the “best travel credit card” tag almost every year for about a decade and so it’s undoubtedly an amazing product that Amex has ever created. Here’s the detailed review of the Amex platinum travel credit card.

Overview

Type

Travel Credit Card

Reward Rate

1% – 8.5%

Best for

Taj Vouchers & Marriott points transfers

USP

Milestone benefits

American Express Platinum Travel Credit Card has been everyone’s #1 choice when looking for a travel credit card because it comes with an attractive value and a relatively easy to reach spend targets.

Currently, one of the best offer you could get is an additional 2,000 MR points as a part of limited period offer when you apply using a referral link.

*** Limited Period Offer: 2,000 Bonus MR Points ***

Apply through the link above to get 2,000 additional Referral Bonus Membership Rewards® points (spend INR 5,000 within 90 days).

Fees

Joining Fee

3,500 INR+GST

Welcome Benefit

10,000 MR Points

Renewal Fee

5,000 INR+GST

Renewal Benefit

Nil

Renewal Fee waiver

Nil

While there are no renewal benefit (or) renewal fee waiver condition, you maybe eligible for the retention benefit based on your profile/spends which may include complete waiver of the fee as well.

Do note that the reward rate takes a little hit when you consider the renewal fee. However, there is a right way to go about it, we’ll discuss that later in the article.

Note: This is platinum travel card and not platinum charge card, which some get confused often, as multiple Amex cards carries the “platinum” tag.

Design

While I’m not a great fan of the Platinum Travel Credit Card’s design, it’s subtle and you wouldn’t be disappointed to have it in hand. The new design is good indeed.

Rewards

SPEND TYPE

REWARDS

REWARD RATE (CASH CREDIT)

REWARD RATE (MARRIOTT/TAJ VOUCHER)

Regular Spends

1 MR on every 50 INR spend

0.50%

~1%

Excluded spends: Insurance, Utilities, Fuel

Rewards don’t expire.

The reward points earned on American Express Platinum Travel Credit Card are ideally meant for Marriott transfers (or) Taj voucher redemptions (according to me), as other options are not attractive enough.

Also note that the MR points earned on plat travel can’t be pooled with other Amex cards, so you can’t redeem for Gold (or) Platinum rewards collection.

While the reward rate on regular spends is not that attractive as seen above, its all about the milestone benefits that makes this card really click!

Note: You’ll unlock 2 benefits on hitting 4L milestone spend, as above.

Note that the above calculation is done by considering “1 MR = 0.50 INR” as we easily get that value by transferring to Marriott or redeem for Taj voucher redemptions.

With Amex Platinum travel card, you may also redeem your MR points for Flipkart vouchers at the rate of “1MR = 0.30 INR” but that’s not a wise option in my opinion.

So, if we consider regular rewards along with milestone benefits, we get a good ~8.5% return on spend post reaching 4L milestone.

What else one can ask for?!

Note: On reaching milestones, you’ll only get 7,500 and 10,000 “bonus” MR points, you’ll then need to call support and ask them to credit remaining points into your account. Gets done in a minute.

Airport Lounge Access

Access Type

Via

Access Limit

Domestic

Amex

8 (2/qtr)

International

Priority Pass

–

Note that you’re eligible only for regular domestic lounge access (for primary cardholders only) but not to the American Express Lounges located in Delhi & Mumbai.

To access Amex proprietary lounges you would need Amex Platinum Charge Card.

While you get complimentary “membership” to Priority Pass for international lounge access, you do-not get any complimentary “access” with it, unfortunately.

My Experience

I’ve been using American Express Platinum Travel Credit Card since past 6 years and it has been an amazing time with the card so far.

I’ve used the Taj vouchers received through amex platinum travel card and other Amex offers to explore some of the beautiful Taj properties (among others) across the country. Here are some of the nice ones that I’ve explored,

Taj Santacruz, Mumbai

Taj Fisherman’s Cove, Chennai

Taj Mahal Palace, Mumbai

Vivanta, Guwahati

Vivanta, Coimbatore

Taj Lands End, Mumbai

Taj Bengal, Kolkata

Taj Connemara, Chennai

Taj West End, Bangalore & few more

Which one is your most-loved or aspirational Taj property? Maybe I can cover the review of it if that interests you.

Other Benefits

Foreign Exchange Markup fee: 3.5% + Service Tax

Amex health insurance benefits (with ICICI Lombard)

Amex Festive Offers

How to apply?

Applying online is the quickest way to get American Express Cards in India.

Currently, one of the best offer you could get is 2,000 additional MR points as a part of the Limited period offer when you apply using a referral link.

*** Best Travel Credit Card in India ***

Apply through the link above to get 2,000 Referral Bonus Membership Rewards® points and even more, check out the link for current bonus gift.

Note: It’s better to apply using your Aadhaar address, otherwise the application might get rejected (or) delayed. If CIBIL is very good it will not ask for income documents.

FAQ’s

1. Is Amex Plat Travel still good in 2024?

Very much it is, as it has the reward rate that is one of the best in industry.

2. What other travel cards can I hold along with Amex Platinum Travel?

Generally most travellers I know have Amex Platinum Travel + Axis Magnus Burgundy + Axis Vistara Infinite. That’s a brilliant combo to fetch overall average reward rate of >10% easily.

3. My address proof is not in serviceable area, what to do?

Amex is strict on that for now (as they know what happens when they don’t follow RBI rules) and so can apply only with valid address proof. Changing Aadhaar address is pretty quick and that works for most.

4. I don’t need a travel card, what other Amex card can I have for rewards?

You should then probably explore the MRCC card. The same can be applied via this referral link.

5. How fast does Amex process the application?

Usually within ~2 days for approval status and another ~3 days for delivery. They’re generally super fast. If it’s your first AMEX Card, it might take additional 1 week depending on various factors.

6. How to get renewal fee waived?

Spending >7L a year usually helps in renewal fee waiver, perhaps you can make use of the spend linked offers post hitting 4L.

Bottomline

Rating: 5/5

American Express Platinum Travel Credit Card with ~8.5% reward rate is one of the highest rewarding Credit Card in India and its a must have in your wallet if you love travel benefits.

That said, the only issue with the card might be the acceptance, but it’s understandable that those who get this card are most likely to use it only at premium hotels and restaurants where the acceptance is generally not an issue.

What’s your take on the American Express Platinum Travel Credit Card? Feel free to share your thoughts in the comments below.

SBICard recently came up SBI Cashback Credit Card, a pure cashback card offering an unbeatable 5% cashback on online spends, outperforming any existing cashback credit card in the country. Looking at the way it is designed, it’s not only a great card for beginners but also for super premium cardholders to spread their spends. Here’s everything you need to know about this must-have cashback credit card in 2024.

Overview

Type

Cashback Credit Card

Reward Rate

Upto 5%

Eligibility

750+ CIBIL Score helps

Best for

5% Cashback on online spends

USP

Higher max. cap. on monthly Cashback

If you’re into entry-level cards and looking for optimising online spends, this is the only card you ever need.

With a 5% earn rate on online spends, it even surpasses super-premium credit cards when it comes to reward rates on online spends.

*** Best Cashback Card of 2024 ***

Fees

Joining Fee

999 INR+GST

Welcome Benefit

–

Renewal Fee / Annual Fee

999 INR+GST

Renewal Benefit

–

Renewal Fee waiver

Spend 2 Lakhs

The not so attractive thing about SBICard in general is that there is no renewal benefit even on payment of the joining fee.

But it shouldn’t matter much for the SBI Cashback Card, as you can anyway get equivalent cashback just with 20K INR online spend.

The design of the SBI Cashback Card looks simple and appealing, as shown above. It also seems that there are slightly different variants of the violet background color, with some cards appearing brighter while others look little darker.

Rewards

SPEND TYPE

Cashback %

Online Spends

5%

Online Spends (>1L per stmt cycle)

1%

Offline Spends

1%

Cashback gets credited within 2 days of stmt. generation

Max Cap: 5,000 INR Cashback limit per stmt cycle (Spend equivalent: 1L Online)

Note: Cashback not applicable on Rent Payments, Fuel Spends, Wallet loads, Insurance, Jewellery, Utilities, gift shops and lot more as mentioned here. (eff. 1st May 2023). Some travel spends are not earning points lately.

For utility/insurance spends, you may anyway buy “Amazon Pay” vouchers on Amazon and pay via Amazon bill payment system, as they have almost all bill payment services under the sun, limits applicable though.

A 5% reward rate on most regular online spends is great without a doubt as the competition hardly gives only 2% or so.

This is not only the best cashback credit card in India but in the entire world, even after the devaluation, as no one ever launched such a simple 5% cashback card in the entire planet.

Cashback Fulfilment

The eligible Cashback gets credited to your card in 2 days after your bill gets generated. You get an SMS notification as well when this happens.

You may as well know your eligible cashback before statement generation by logging into your SBICard Netbanking account.

Lounge Access

The SBI Cashback Credit Card initially offered airport lounge access when it was launched. However, this benefit was later revoked, and the card no longer includes lounge access.

I think it’s fair, given that the USP of the card, which is 5% cashback on online spends stays intact for 1L monthly spends.

Other Benefits

Fuel surcharge waiver: 1% Fuel Surcharge Waiver across all petrol pumps in India (Txn size: Rs. 500 – Rs. 3,000)

While the SBI Cashback Card doesn’t offer many additional benefits, it’s important to note that the core benefit of cashback on online spends alone is sufficient reason to hold the card.

Credit Limit Issue

One of the issue about SBI Cashback card is that it gives ultra low credit limits, as low as 10,000 INR.

This usually happens when you have multiple SBI Credit Cards, as SBICard isn’t generous with credit limit especially when you get closer to 5L credit limit across your SBI Cards.

So it applies to all SBI Cards when you apply for a 2nd card and it’s not limited to just Cashback card.

I’m sure of this because I myself got <50K INR credit limit on Cashback card (2nd card) while my friend got ~3L Credit limit (new to SBICard).

But you may anytime call SBICard support and ask to transfer some of the limit from the existing card to the new one. I did the same by transferring some limit from SBI Aurum Card and the updated limit reflects instantly.

My Experience

I applied online and got the card approved in about 10 days (with virtual card ready to use) and it took another 7 days for physical card delivery.

The cashback system is quite simple and works flawlessly, as expected. If you wish to cross verify the txn type and cashback, you may find it via spend analyzer on desktop. Note that the spend analyser on SBICard mobile app shows wrong txn type, for unknown reasons.

Should you Apply?

If you’ve good amount of online spends, there is no reason not to apply for the SBI Cashback Credit Card.

However, if your spends are mostly offline, you may perhaps explore the SBI SimplyClick Credit Card which can offer a decent ~3% return on 2L annual spends.

SBI Cashback Credit Card can be applied only online through their newly developed Sprint onboarding system. If you’re new to it, this article may help: SBICard Sprint Application Process.

*** Best Cashback Card of 2024 ***

Bottom line

Rating: 4.7/5

With 5% Cashback literally on almost all online spends, SBI Cashback Credit Card is indeed the best cashback credit card in India.

I never thought SBICard would go this aggressive on entry-level cards. While this is great, I wish to see such aggressiveness on their super premium vertical as well.

However, remember that 5% cashback upto 5K INR a month is not going to last long. It’s more of card acquisition model and so expect it to be “trimmed” as soon as the issuer gets sufficient users on the platform.

We’ve already seen the 1st round of devaluation eff. 1st May 2023 and looking at how lucrative the card is, we may expect the 2nd round of devaluation anytime. Until then,

Make hay while the sun shines!

Do you have SBI Cashback Credit Card? Feel free to share your thoughts & experiences in the comments below.

SBI SimplyClick Credit Card is one of the very few credit cards in India that has pretty good reward rate on regular spends for beginners.

While it used to be one of the most sought after entry-level credit card in the past because of the 10X rewards, it’s still a good pick in it’s current form.

Overview

Type

Cashback Credit Card

Reward Rate

0.20% – 2%

Annual Fee

499 INR+GST

Best for

Online spends upto 2 Lakhs a year

USP

Milestone benefits

SBI SimplyClick Credit Card has been the only best entry-level credit card until the launch of SBI Cashback Credit Card.

While SBI Cashback Credit Card is primarily meant for online spends with the possibility of getting devalued anytime, SBI SimplyClick Credit Card is evergreen and could get you a decent reward rate of over 2% on annual spends of 2 Lakhs, thanks to the milestone benefit, which we’ll see shortly.

Fees & Charges

Joining Fee

499 INR+GST

Welcome Benefit

500 INR Amazon eVoucher

Renewal Fee

499 INR+GST

Renewal Benefit

–

Renewal Fee waiver

Spend 1 Lakh

While Amazon voucher takes care of the fee for 1st Year, annual spend of just 1 Lakh is sufficient for the renewal fee to be waived off, which is easy for most cardholders in the segment.

Design

SBI SimplyClick Credit card is probably one of the few entry-level cards that also looks good in terms of design.

Earlier it used to be in matt finish and now it’s being issued with a shiny front face that looks more appealing.

Rewards

SPEND TYPE

CASHBACK %

Online Spends

~1%

Offline Spends

~0.20%

Select merchants (10X)

~2%

Points Validity: 2 Years

No points on discounted products on Flipkart/Amazon

Note that the point value on SBI SimplyClick Credit Card has dropped from 25ps to 20ps recently.

But the good thing is that we can redeem points for Amazon Pay eVouchers which is almost cash equivalent.

The SBI SimplyClick Credit Card was quite popular in the past because of it’s 10X rewards especially on Amazon for obvious reasons but that it no longer available.

While the current partners are decent, the drop in point value further makes it less attractive than it used to be.

Milestone

SPEND REQUIREMENT

MILESTONE BENEFIT

VOUCHER TYPE

1 Lakh

2,000 INR

Cleartrip/Yatra

2 Lakh

2,000 INR

Cleartrip/Yatra

Yatra Voucher: Can be redeemed for flights/hotels

Cleartrip Voucher: Can be redeemed only for flights

Voucher Validity: 4 months

Voucher is usually triggered in ~2 weeks of reaching the milestone.

This is a neat and simple benefit which is useful for travellers. While they used to have only Cleartrip Voucher in the past, it seems they’re now offering Yatra Vouchers.

So by reaching the milestone through typical online spends, one could easily get a sweet reward rate of 3% which is great for this segment.

My Experience

I was using SBI SimplyClick Credit Card in the past, before moving to SBI Prime for few years and then to Aurum.

Back in time I got the Cleartrip vouchers which I used for a stay in Malaysia. The redemption was quick and simple.

And I recently downgraded my Aurum to Simplyclick once again to primarily retain the credit limit on the card.

And for the milestone spends, this time I got the Yatra Vouchers. Hope the redemption is as simple as it used to be on Cleartrip.

While I haven’t used the Yatra voucher, from t&c it appears to be a straightforward process to redeem them as well.

How to Apply?

SBI SimplyClick Credit Card can be applied online which uses the latest sprint application system for quicker processing.

If you’re new to the sprint application process, this article may help: SBICard Sprint Credit Card Application Process.

Bottomline

Cardexpert Rating: 4/5

The SBI SimplyClick Credit Card is great for beginners who can spend 1L (or) 2L a year, at offline stores or online.

If your annual spends are over 2 Lakhs and if they’re primarily online then you should instead go for the SBI Cashback Credit Card that offers lucrative 5% Cashback on online spends.

While the Cashback Card is the hot pick for beginners since 2022, it may anytime go for the next round of devaluation.

Nevertheless, SBI SimplyClick Credit Card also serves as a solution to hold the credit limit until the next premium credit card arrives.

Do you hold SBI SimplyClick Credit Card? Feel free to share your thoughts in the comments below.

AU Bank offers various credit cards based on spending habits and lifestyle. From the plethora of AU Bank credit cards, you can choose the one that is best suited for you. Here is the list of all AU Bank credit cards and their main features.

Fee for reissue of lost/damaged/stolen credit card

Rs.100

Goods and Services Tax (GST)

18%

Late Payment Charges

Outstanding amount and Fee:Less than Rs.100: NILRs.100 to Rs.500: Rs.100Rs.501 to Rs.5,000: Rs.400Rs.5,001 to Rs.20,000: Rs.500More than Rs.20,000: Rs.700

How do I reach the AU Bank concierge desk?You can reach the AU Bank concierge desk by calling the toll-free number, 18002100298. You can also call 022-42320298 to reach the concierge desk.

What is the foreign currency mark-up fee for the AU bank credit cards?Altura, Altura Plus – 3.49%, Vetta – 2.99%, Zenith – 1.99%, and LIT – 3.49%

How old should the add-on credit cardholder be?The add-on cardholder has to be more than 18 years old.

Which e-mail ID can I write to for queries regarding the AU Bank credit cards?You can write to creditcard.priority@aubank.in and clarify your doubts on the AU Bank credit cards.

How much GST will be applicable on an AU Altara Plus Credit Card?18% GST will be levied on fees and other charges on an AU Altara Plus Credit Card.

What is the joining fee of the AU Bank Zenith Credit Card?There is no joining fee for AU Bank Zenith Credit Card.

What is the maximum limit for AU Bank credit cards?On AU credit cards, there is no set limit. It is determined by the applicant’s income and CIBIL score. Individuals with a high income and a high CIBIL Score are more likely to be given a large credit limit. To secure fast approval for the AU Bank Credit Cards, the applicant must have a CIBIL Score of 750 or higher.

What is the minimum and the maximum age limit to avail an AU Bank Credit Card?To avail an AU Bank Credit Card, the applicant should be under the age limit between 21 years to 60 years.

What are the documents required to avail an AU Bank Credit Card?To apply for a credit card from AU Bank, you have to submit several documents like Permanent Account Number (PAN) card, Aadhar card, passport, driving licence, Voter ID, electricity bill, last six months’ salary slips, Income Tax Returns (ITR) of last two years, and birth certificate.

American Express offers various credit cards based on spending habits and lifestyle. From the plethora of American Express Platinum Credit Card, you can choose the one that is best suited for you.

Enjoy flexible spending power with “no pre-set limit” that keeps adjusting automatically based on your financials, spend pattern, credit record and account history

Complimentary membership to Elite tier programmes such as Hilton HonorsTM Gold Status, Taj InnerCircle Silver tier, Marriott BonvoyTM Gold Elite Status, Radisson Rewards Gold Elite Status, Taj Epicure and Complimentary access to over 1,200 airport lounges including the Centurion® Lounge and the International American Express lounges, or visit one of our partners including Delta Sky Club® when flying Delta or a Priority PassTM lounge

Special invitation to a host of events, fine dining privileges at renowned gourmet restaurants, complimentary tee offs at over 30 premier golf courses & two complimentary golf lessons every month at 16 golf courses across India

SBICard recently launched a dedicated fuel credit card in association with Bharat Petroleum Corporation Limited and this article is all about SBI BPCL Fuel Credit Card . The features mentioned on the card is kinda bit confusing because of lots of terms and conditions but here we’re to breakdown the numbers.

Overview

Type

Fuel Credit Card

Reward Rate

Upto 3%

Annual Fee

1,000 INR+GST

Best for

BPCL Spends

USP

Good redemption options

I would never suggest fuel credit cards to anyone and SBICard support is very poor in that matter. So, stay away!

Joining Fees

Joining Fee

500 INR+GST

Welcome Benefit

2000 Points (Rs.500 worth of fuel)

Renewal Fee

500 INR+GST

Renewal Fee Waiver

Nil

Your joining fee is only partly offset by the welcome benefit (except GST). That aside, you don’t get renewal fee waiver with this Card, which is otherwise present in Axis Indian Oil & Citi Indian Oil fuel credit Cards.

The “13X Reward Points on fuel purchases at BPCL” simply means 13 Points and as the value of each point is Rs. 0.25, effective value out of 13X points = 3.25%. Now lets say you fuel for Rs.1000 and see how much you save.

Fuel Charge at BPCL: 1000 INR

-10 INR (1% Surcharge)

+10 (1% Surcharge Waiver)

-1.8 (18% GST on surcharge)

+32.5 (13X Points)

Total Savings = 30.7 INR Equivalent (3% value)

So, in simple words, you can save max. Rs.325 per month (1300 points max per billing cycle) if you spend ~10,000 INR (may differ if you cross this limit) exactly ON FUEL but the effective savings maybe lot more if you’re currently using a credit/debit card that charges you surcharge.

Apart from the above, you can also get 5X points by spending on certain categories, which will save you 1.25% (5X points) which is OKAY if you don’t have cards like SBI Prime which has wonderful reward rate on many categories.

Conditions:

SBI Surcharge on Fuel: 1% or Rs.10 whichever is higher (txn value Rs.500-Rs.4000)

Max Surcharge Waiver: Rs.100/m (Spend: Rs.10,000/m)

Max txn value per swipe: Rs.4000

Important Note: If you note the first point, the above savings wont work if you fuel BIKES, which is usually in Rs.500 range. Hence, holds good for car fuel spends between Rs.1000 to Rs.4000.

The limits above are in place to avoid charges by commercial vehicle users. Ideally, this is an acceptable limit for the card as its primarily positioned for beginners with BPCL spends.

Bottom line

Rating: 3.5/5

Its good to see banks come up with dedicated Fuel cards but i wish it could be made even more simple. For example, I always prefer to use Amex cards at HPCL pumps so i get NO surcharge at all – peace of mind.

That aside, overall its a decent card for those who’s getting started with credit cards or for those who like a good value back on fuel charges. If you’re looking for even better fuel card, do check out the list of Best Fuel Credit Cards in India.

What’s your take on the new SBI BPCL partnership? Feel free to share your thoughts in comments below.